The ESRS Just Got Simpler: What You Need to Know About the 2025 Revisions

On 30 July 2025, the European Financial Reporting Advisory Group (EFRAG) published a significantly revised Exposure Draft of the European Sustainability Reporting Standards (ESRS). This marks the most substantial update since the ESRS were adopted in 2023.

The revisions apply to all 12 sector-agnostic standards and are part of the European Union’s Omnibus Simplification Package, aimed at making sustainability reporting under the Corporate Sustainability Reporting Directive (CSRD) more practical, streamlined, and aligned with global standards.

Why are the ESRS being amended?

EFRAG initiated the revisions in response to feedback from companies preparing to report under CSRD–particularly smaller firms and first-time reporters–who raised concerns about the cost and feasibility. The updates are also part of the European Commission’s broader effort to reduce administrative burden without compromising on relevance, comparability, or alignment with the European Green Deal.

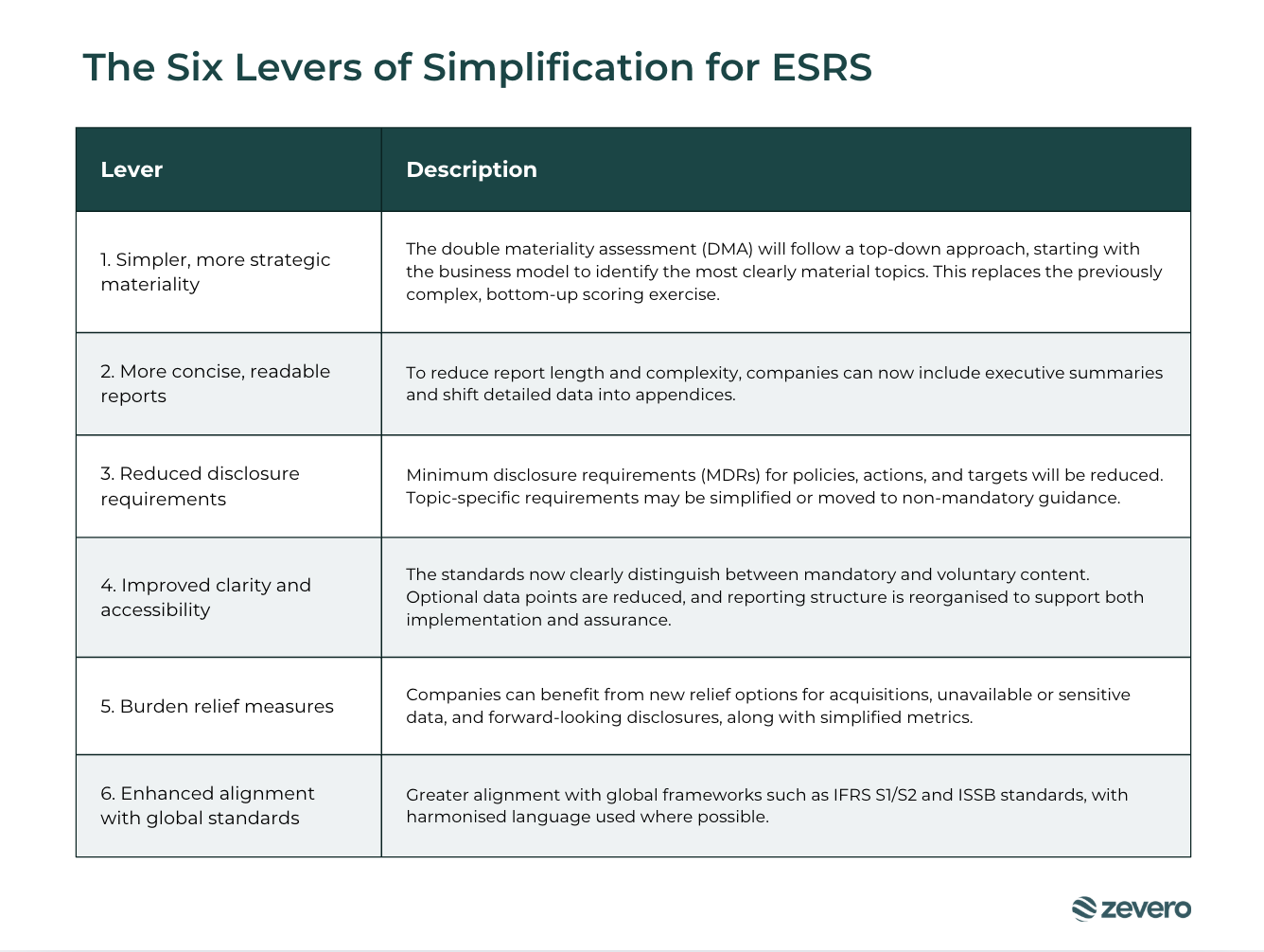

To achieve this, six strategic simplification “levers” were applied across all 12 cross-cutting and topical standards:

- Clarifying content and structure: Improved consistency in formatting, language, and layout to enhance usability.

- Confirming materiality requirements: Reaffirmed that disclosures are only required when a topic is material, and simplified the materiality assessment process.

- Recalibrating the content: Reduced the number of required datapoints and removed all voluntary disclosures.

- Reducing granularity of requirements: Consolidated overlapping or excessively detailed requirements.

- Introducing phase-ins and reliefs: Expanded transitional reliefs and cost/effort exemptions, with clearer guidance on how and when these may be applied.

- Improving interoperability: Strengthened alignment with frameworks such as the ISSB IFRS S1 & S2.

Collectively, these levers aim to retain the ESRS’s core intent: ensuring comprehensive and comparable sustainability reporting while making the framework more practical and proportionate, especially for SMEs and new reporters.

Key updates across standards

The most noticeable shift is the scale of simplification:

- Mandatory datapoints reduced by 57%

- Total datapoints reduced by 68% due to the removal of voluntary (“may”) disclosures

- Over 55% reduction in total length of the standards

Each of the ten topical standards (E1–E5, S1–S4, G1) has been updated. Notable changes include:

- E1 Climate Change: Clearer disclosures on transition plans, Scope 1‑3 emissions, energy mix, and removals; greater alignment with 1.5 °C pathways and SBTi methodology

- E2–E5 Environmental Standards: Objectives and disclosures have been streamlined and merged; EU policy references updated

- S1–S4 Social Standards: Harmonised structure across workforce, value chain workers, affected communities, and consumers; stronger human rights alignment

- G1 Business Conduct: Streamlined focus on ethics, anti‑corruption, lobbying, supplier conduct, and whistleblowing, with flexibility only to report on material topics

In addition to these content updates, the draft introduces structural simplifications designed to improve clarity and consistency across standards:

- Merged disclosure objectives: Previously separate paragraphs on impacts, actions, risks, and financial effects have been consolidated

- Harmonised layout: A consistent reporting logic now applies across all topical standards

- Executive summary option: Companies may now include a high-level overview at the start of their sustainability statement, with detailed data moved to appendices where appropriate

These structural changes aim to make reporting more intuitive and implementable, particularly for first-time reporters.

Structural overhaul: New format

To reduce duplication and improve clarity, the revised ESRS merge previously separate objectives on impacts, actions, risks, and financial effects into unified disclosure paragraphs. Companies are now required to report only on subtopics deemed material via a top‑down materiality assessment, moving away from overly granular scoring exercises.

Other structural changes include:

- Consistent reporting logic across all topical standards

- Materiality-driven disclosures only where relevant

- Optional executive summary at the start of the sustainability statement

- Appendices for detailed datapoints, reducing the burden on the core report

These changes aim to reduce complexity while maintaining accountability and alignment with the broader sustainability reporting ecosystem.

Proposed amendments to the Impact Materiality Assessment

EFRAG has introduced a significant clarification to how companies should assess impact materiality under ESRS 1. One of the most common challenges in the original standards was the so-called “gross vs. net” issue: whether organisations could take into account existing mitigation or prevention measures when determining the severity and likelihood of potential negative impacts.

Under the proposed amendments, companies would be allowed to consider the outcomes of any mitigation or prevention actions implemented before the impact occurred, so long as there is “supportable evidence” that these actions reduce either the severity or likelihood of future impacts.

This clarification has two important implications:

- Improved consistency in assessments: Companies will now have clearer guidance on how to evaluate sustainability impacts, enabling more consistent materiality assessments across sectors and organisations.

- Recognition of proactive risk management: Organisations that have already implemented strong sustainability controls can reflect their progress in their impact assessments, rather than being penalised for having addressed risks in advance.

This proposal helps to close a long-standing gap in the ESRS and aligns the framework more closely with the realities of corporate sustainability planning and risk mitigation. It also supports a more accurate portrayal of where an organisation stands in terms of potential environmental and social impacts.

Options for reporting financial effects

New options have been proposed for disclosing the financial implications of sustainability risks and opportunities under ESRS 2. The draft outlines two approaches:

- Require quantitative disclosures, but include reliefs allowing qualitative substitutes when data is not available, drawing from ISSB practices.

- Make qualitative disclosures mandatory, with quantitative information optional.

The approach ultimately selected will influence the systems and data infrastructure companies need to have in place to comply with CSRD.

Legislative constraints: What won’t change (yet)

Not all requested changes could be addressed in the revised draft. Several issues remain unresolved because they require amendments to the CSRD itself and must be negotiated and adopted by the European Parliament, Council, and Commission.

These “Level 1” items include:

- The definition of value chain for financial institutions

- Whether financial holding companies must consolidate subsidiaries

- Potential exemptions for confidential or sensitive information

- Clarification of what qualifies as a 1.5°C-compatible transition plan

These areas will continue to be discussed at the EU legislative level and may be updated through future amendments.

What should companies do now?

With the public consultation open until 29 September 2025, organisations should take the following steps to prepare and respond:

1. Revisit your materiality assessment

Apply the new guidance around mitigation and prevention measures when assessing potential impacts.

2. Evaluate your readiness for financial disclosure

Assess your current systems and reporting capabilities to determine whether they’re better suited to the qualitative or quantitative disclosure option. This will help you prepare regardless of which option EFRAG adopts.

3. Review and realign your ESRS structure

Conduct a gap analysis against the revised draft, taking note of the eliminated datapoints, merged disclosure objectives, and structural changes.

4. Participate in the public consultation

Submit feedback to EFRAG. Use the consultation window to advocate for further clarity or raise concerns on key revisions.

5. Monitor upcoming legislative changes

Stay up to date on developments regarding Level 1 amendments that may impact your reporting obligations in future years.

Timeline and next steps

- Public consultation open: 31 July – 29 September 2025

- EFRAG final recommendations to European Commission: End of November 2025

- Revised ESRS adopted via Delegated Act: Late 2025

- Effective date: Applies to financial years beginning on or after 1 January 2026 (first reports published in 2027)

These revisions mark a significant evolution of the European Sustainability Reporting Standards. While the standards remain rigorous, the proposed updates reflect EFRAG’s intent to balance transparency with practicality, especially for companies reporting for the first time under the CSRD.

How can companies stay informed?

Zevero will continue to track developments and share further analysis of the ESRS once the final standards are adopted. For more information, read our earlier update on the EU Omnibus Package, or reach out to our experts.

.webp)